Compound Interest

Working for you or against you

“Compound interest is the eighth wonder of the world. He who understands it, earns it. He who doesn’t, pays it.”

Albert Einstein

Compound interest is interest that is earned on both the initial sum as well as the interest earned over a given period, and those periods reset, usually every year. For example, say you invest $1000 and earn 10% interest, in the first year you would earn $100 in interest. The second year, the period resets and you now earn interest on $1100. After the second year, you would have $1210. After the third year, $1331. As you can see, the total is compounding every year, and as time passes the total will grow exponentially larger. This is different from simple interest. Simple interest would be $100 earned every year on the initial $1000 investment.

The power of compounding can cut both ways. Credit cards are notorious for trapping people in a debt snowball. It’s made worse by the fact that our brains do not naturally comprehend compound interest and we are led to believe that the minimum payment is all we need to pay in order to service the debt. If we actually read our credit card statements we would know that that is not the case, but who reads the fine print?

Example

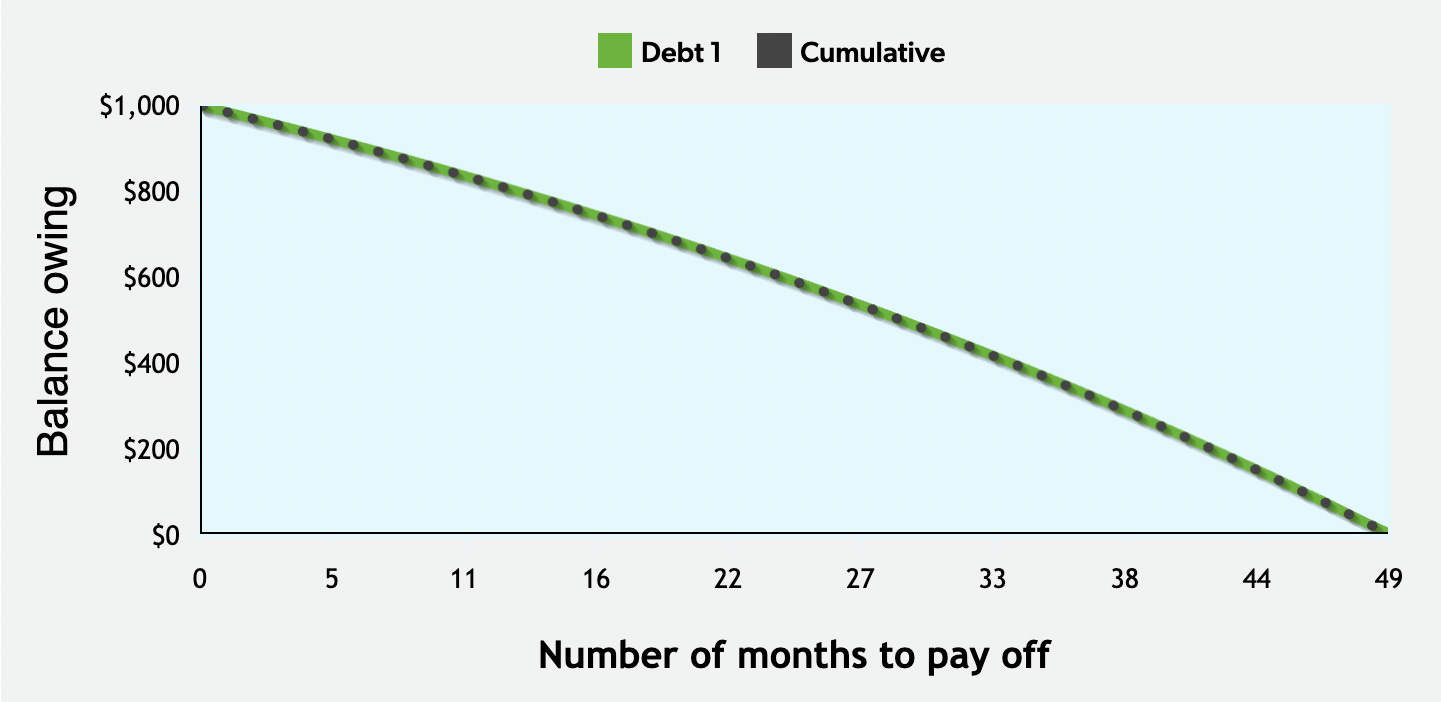

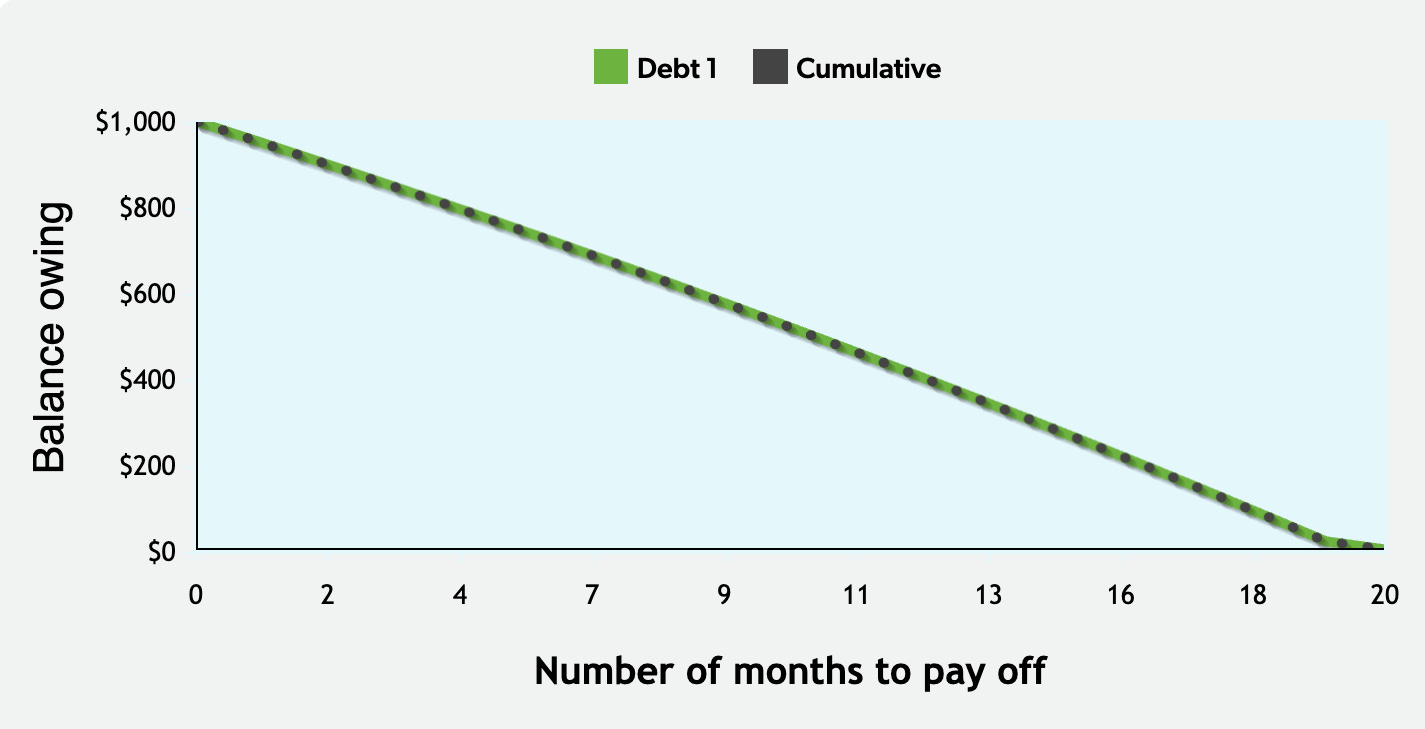

Let’s say you have $1000 in debt on a credit card with an interest rate of 18%, your minimum payment is $29. It would take you more than 4 years to pay off that debt, because compound interest is working against you. If you remove the interest expense on this debt, it would only take you 2.8 years to pay off the debt. If you were to double your payments to $60, with interest, it would only take 1 year and 8 months to pay off the debt. This is the power of compound interest working against you.

$1000 debt, $29 minimum payment

$1000 debt, $60 payment

If you would like to play around with this tool and put in your own numbers, please visit Get Smart About Money

Now let’s look at how compound interest can work in your favour. The most important inputs for compounding to work for you are time and rate of return. The rate of return (interest rate) has limited upside and you cannot control how your investments will perform, the best you can do is pick the right investments that give you the best upside and lowest risk. The input you can control is time. No, you cannot actually control time, what I mean is you can control how long you hold an investment.

“The first rule of compound interest is to never interrupt it unnecessarily.”

Charlie Munger

The best way to take advantage of compound interest is to get started as soon as possible and never interrupt the compounding process unnecessarily.

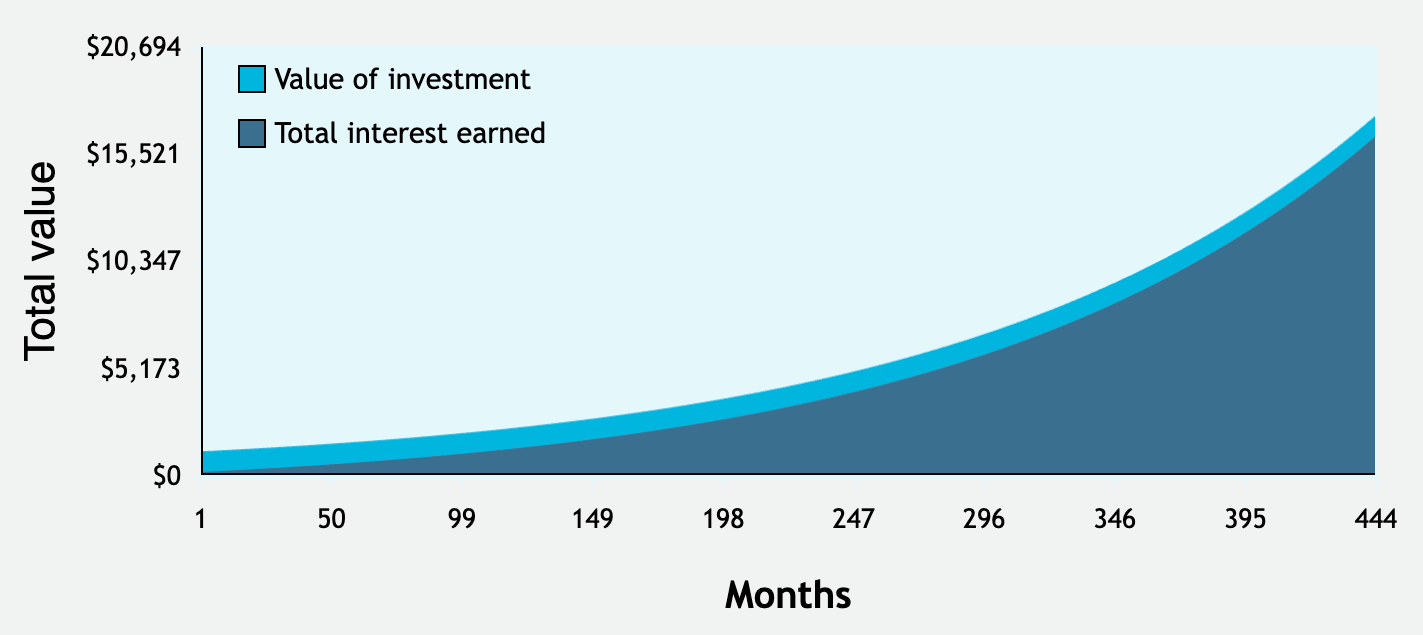

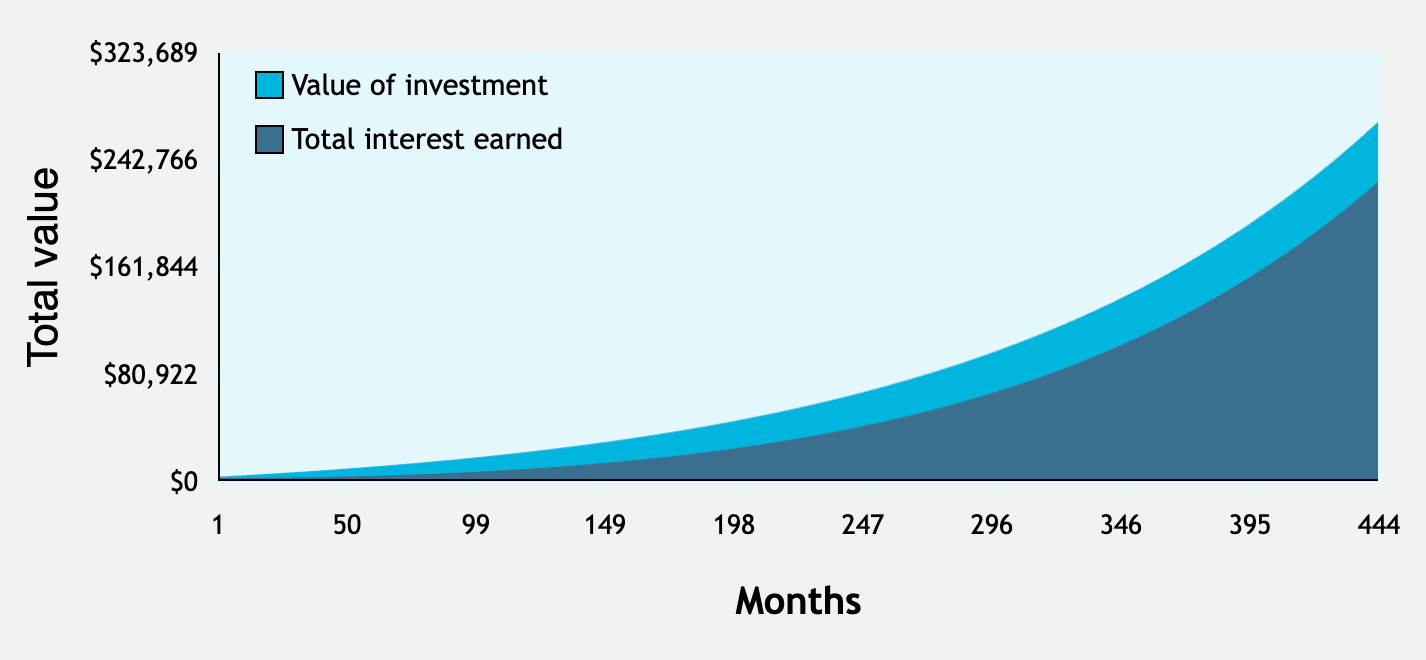

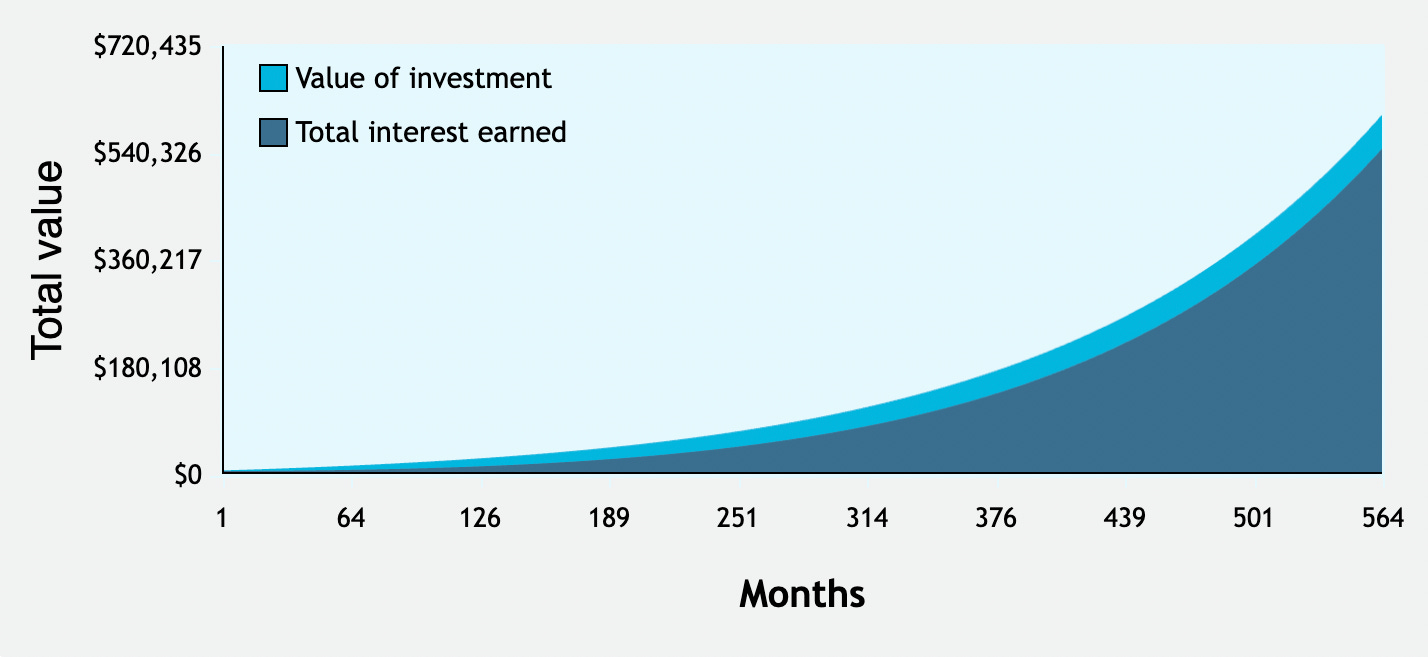

Let’s look at the power of compounding working in your favour. Let’s say you invest $1000 on your 18th birthday and your investment is going to grow at a rate of 8% per year. By the time you are 55 that $1000 would now be worth $17,245.

By 65 it would be worth $37,232.

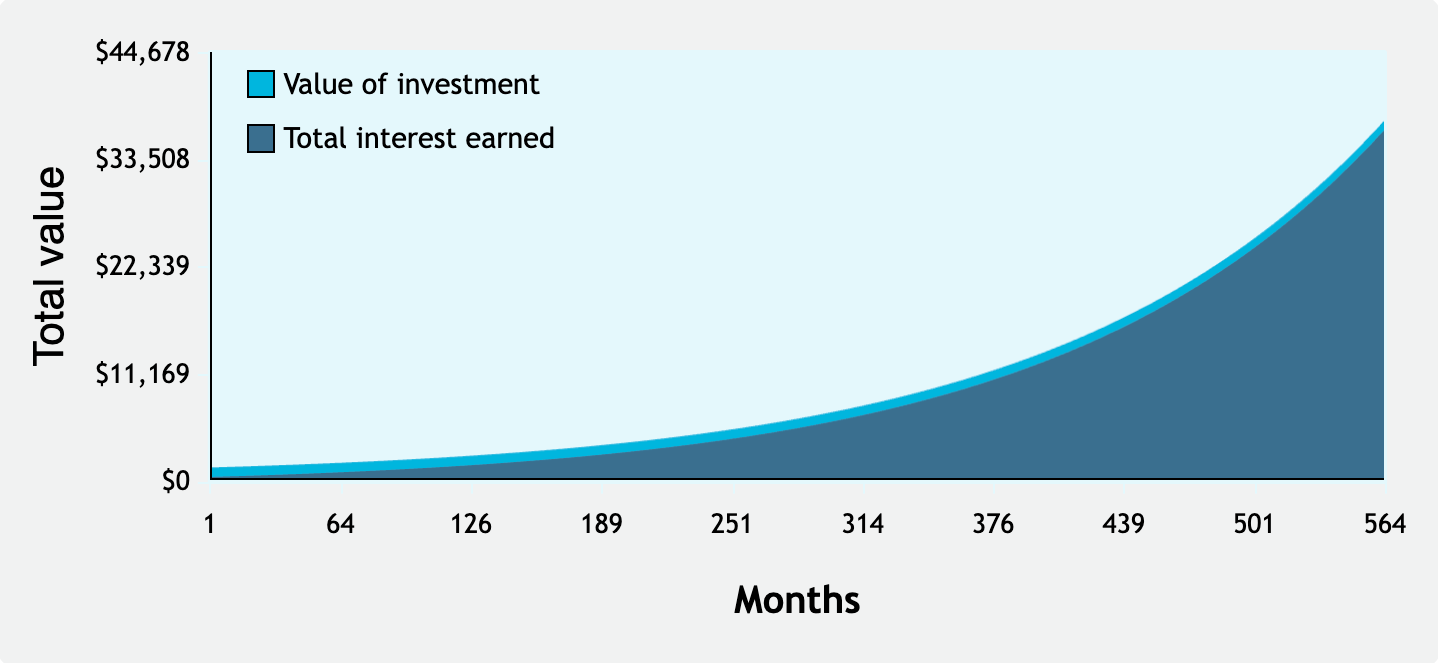

If you were to regularly contribute to you investments on a monthly basis, your savings would grow much larger over time.

If you saved an additional $100 per month, by age 55 your investments would grow to $269,740.

By age 65, your investments would be worth $600,362.

The two variables you can control are time, how long you invest your money, as well as how much you save and how often. Obviously, the more you save and the longer you invest your money, the larger your money will grow. The other variable in the equation is the rate of return, which you do not have control over. But you can control where you invest your money with an idea of the rate of return you can expect. I will dive deeper into expected returns in a future post. For now, wrap your head around compound interest. Play around with a compound interest calculator like the one found here Compound Interest Calculator. Imagine what the power of compound interest could do for you and your future.